Unifying the Global Money Movement Rails

How we reduced customer support tickets by 50% by abstracting banking infrastructure complexities (SWIFT, ACH, SEPA) into a user-centric "Single Send" experience.

Problem

Cross-border payments were a "black box" with high fees and 24% drop-off rates.

Role

Lead Product Designer (Strategy, IA, Design Systems).

Complexity

SWIFT/ACH rails, compliance checks, and 800ms API latency.

Action

Built a rail-agnostic routing engine and "Single Send" flow.

Result

-50% support tickets, +18% funnel conversion.

Situation: The Global Liquidity Gap

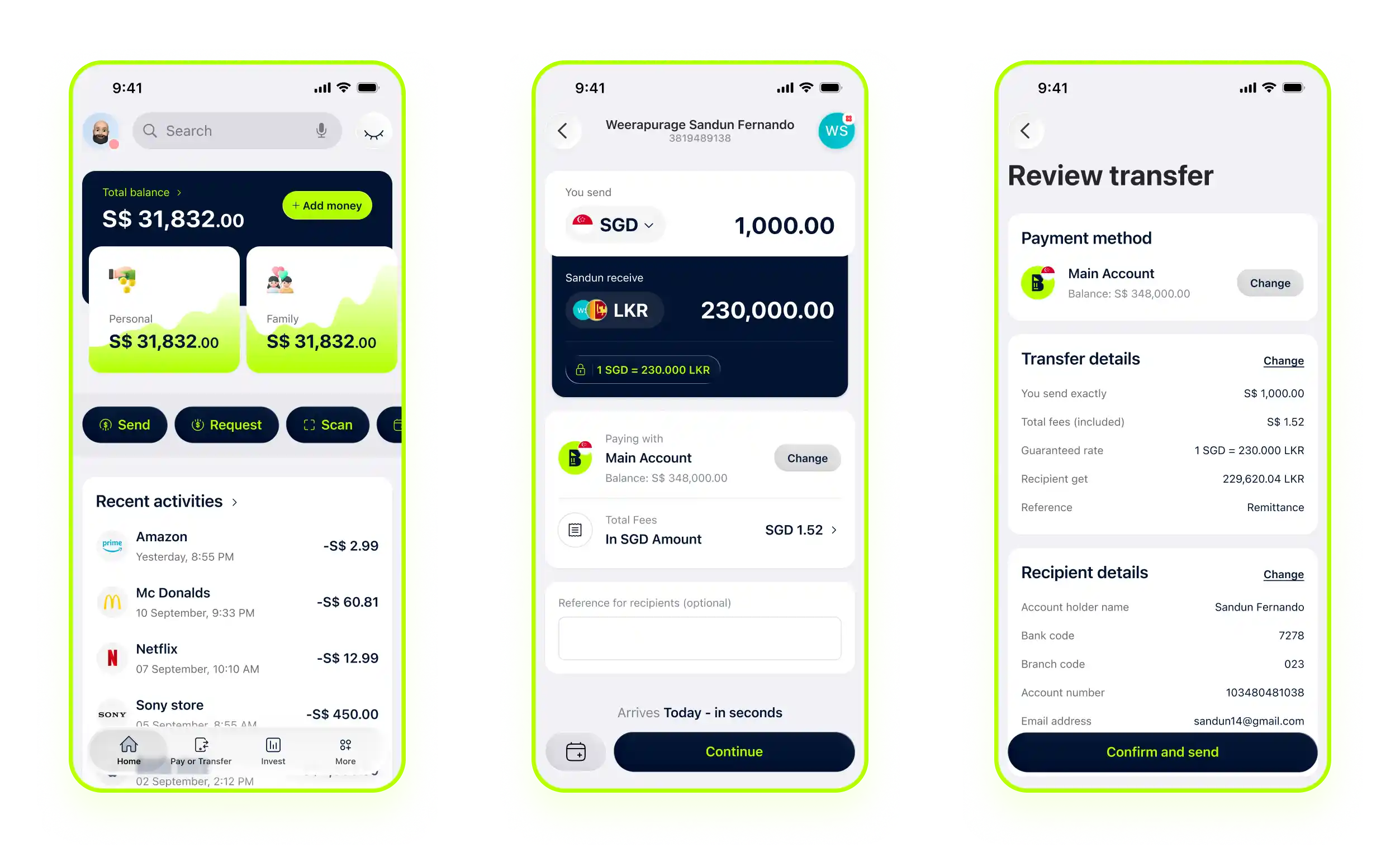

International money movement is notoriously broken. For users, it's a "black box" of hidden intermediary fees ($25-$50), unclear delivery times, and complex jargon like SWIFT, IBAN, and BIC.

This lack of transparency created massive user anxiety, leading to a 50% support ticket volume purely for "Where is my money?" queries. Failed transfers due to incorrect recipient data further eroded trust.

Business Problem

High operational costs due to support volume, high churn from failed transfers, and a 24% drop-off at the rail selection screen.

Legacy Experience Audit

- Total "Black Box" (No status updates)

- Hidden Intermediary Fees ($25-$50)

- Complex "Banking Jargon" (IBAN, BIC, SWIFT)

- Zero Error Recovery (Fail = Money stuck 10 days)

Task: Abstracting Banking Rails

My mission was to bridge the gap between bank-grade complexity and user-centric simplicity. This meant moving away from "Select a Rail" (ACH vs. Wire) and towards a mental model centered on Relationship and Urgency.

Build Trust

Eliminate the "Black Box" by providing real-time status and fee transparency.

Reduce Friction

Automate routing decisions to prevent user choice paralysis and errors.

Deflect Support

Provide self-healing error recovery and predictive delivery timelines.

Discovery Phase

Understanding "The Bleed"

Activity 1: The Affinity Wall

"I don't know the difference between ACH and Wire. What if I pick the wrong one and lose money?"

"Why does it feel like I'm filing taxes just to send $50?"

"Routing Number? Swift Code? I just have their email address."

"I use CashApp because it just asks 'How much?'. I want that here."

"Just make it fast. I'll pay extra."

Heuristic Evaluation (Nielsen's 10)

System provided zero feedback during the 3-5 day settlement window. Users felt the money had "vanished".

Used terms like "IBAN", "SWIFT", and "BIC" without explanation, confusing non-expert users.

No validation on input fields allowed users to send money to invalid account numbers, causing failed transfers.

Data Validation: Quantifying the Friction

We cross-referenced the qualitative feedback with analytics. The results were shocking: Complexity was a bigger blocker than Fees.

- 45% dropped off due to "Confusion" (User Testing).

- Only 15% dropped off due to "Cost".

Ideation Phase

Brainstorming the "Rail-Agnostic" Flow

How might we hide the banking complexity while keeping the compliance flexibility? We used the "Crazy 8s" method to sketch solutions.

Sketch Idea: "The Magic Input"

"The system should decide the rail (ACH/Wire) based on the amount."

The "Aha!" Moment

We realized we didn't need to ask the user how they wanted to send money. We only needed to ask When they needed it to arrive.

The New Logic

IF (Amount < $5000) -> Use P2P (Instant)

IF (Amount > $5000) -> Use Wire (Same Day)

ELSE -> Use ACH (Free)

The Solution Architecture

Rail-Agnostic Routing Engine

To solve the "Mental Model Mismatch", we inverted the control flow. Instead of asking users to choose a rail (Wire vs ACH), we built a middleware logic that selects the best route based on specific constraints.

-

1. Algorithmic Selection

Engine checks: Amount > $5k? Is it a weekend? Is destination eligible for Instant P2P?

-

2. Compliance Handshake

Real-time sanctions screening (OFAC) happens before the user hits submit, preventing stuck funds.

// Smart Routing Logic

function getBestRoute(amount, urgency) {

if (urgency === 'instant') {

return RTP_NETWORK; // Real-Time Payments

}

else if (amount > 5000) {

return SWIFT_WIRE; // High Value Protection

}

else {

return LOCAL_ACH; // Lowest Cost

}

}

Action: Bridging the Divide

Transforming infrastructure into experience

Phase 1: Discovery & Alignment

I orchestrated a 3-phase discovery and design process to de-risk the solution.

Assumptions Mapping

I gathered Product and Engineering to map out what we thought users knew about banking rails vs. reality.

Outcome

Stakeholders overestimated user literacy. We agreed to hide technical terms (ACH/Wire) and replace them with "Standard" and "Instant".

Competitor Benchmarking

Competitors (Wise, Revolut) don't make users choose rails. They ask "Who?" and "How much?" first.

- Used data to get buy-in

- Validated flow restructure

Phase 2: Defining the Mental Model

Activity: Open Card Sorting (Remote via Maze). I asked 30 participants to group 20 distinct transaction scenarios.

Outcome

Users grouped by Relationship (Family vs. Business) and Urgency, never by technology. This validated the decision to remove the "Select Transfer Type" screen entirely.

Phase 3: Accessibility-First Design

The "Smart Routing" Logic: I designed a Progressive Disclosure interface. We only reveal complexity if necessary. The system defaults to the cheapest option, allowing users to toggle to "Fastest" if needed.

WCAG 2.1 AA Implementation

Instant Transfer Unavailable

We can send this via Standard delivery instead.

Designing for "The Worst Case"

In cross-border payments, the "Happy Path" is easy. The real design work happens at the edge cases: sanctions hits, intermediary bank delays, and failed recipient validation.

Fee Transparency

Guaranteed FX rates and upfront breakdown of intermediary fees to eliminate "Post-Transfer Shock".

Predictive Delivery

AI-driven settlement prediction based on corridor history and bank cut-off times.

Sanctions Pre-Check

Real-time screening against OFAC/AML lists *before* fund commitment to prevent stuck money.

"By surfacing the compliance check as a deliberate step, we increased perceived security and reduced anxiety."

Designing for "The Worst Case"

In cross-border payments, the "Happy Path" is easy. The real design work happens at the edge cases: sanctions hits, intermediary bank delays, and failed recipient validation.

Fee Transparency

Guaranteed FX rates and upfront breakdown of intermediary fees to eliminate "Post-Transfer Shock".

Predictive Delivery

AI-driven settlement prediction based on corridor history and bank cut-off times.

Sanctions Pre-Check

Real-time screening against OFAC/AML lists *before* fund commitment to prevent stuck money.

"By surfacing the compliance check as a deliberate step, we increased perceived security and reduced anxiety."

Strategic Design Decisions

Rail-Agnostic Routing

Instead of asking users to choose "ACH" or "Wire," we ask for "Amount" and "Urgency." The system selects the best rail behind the scenes.

Progressive Disclosure

Hide technical recipient requirements (IBAN/BIC) until the user enters the destination country, reducing initial cognitive load by 40%.

Plain Language Copy

Replacing banking jargon with user-centric outcomes (e.g., "Cheapest" vs. "Fastest") directly impacted the 18% conversion lift.

The Design

Optimized for cross-border transactions

Send funds across borders with real-time exchange rates and no hidden fees.

- Transparency and security.

- By mentioning "initiation to deposit," we provide a clear roadmap of the money's journey.

Leadership & Collaboration

Product (PM)

Partnered on corridor-specific localization strategy and prioritising high-value high-friction markets.

Engineering

Worked with backend teams to optimize API response times (800ms) and implement optimistic UI patterns.

Compliance

Aligned on OFAC/AML screening triggers to ensure 100% regulatory adherence without blocking user flow.

Ops & Support

Reduced manual ticket handling by 50% through automated status updates and self-healing recovery flows.

The Result

Impact & Verification

"Select Transfer Type" drop-off eliminated.

Saved ops team effort approx 20 hours/week.

Design system components adopted widely.

Support Volume Impact

| Metric | Before | After |

|---|---|---|

| Funnel Drop-off Rate | 24% | 6% |

| Task Success Rate | 78% | 98% |

| Monthly Support Tickets | ~1,200 | ~600 |

| Recovery Workflow | Manual (Ops) | Self-Healing |

| Accessibility Score | 72 / 100 | 98 / 100 |

What Users Said

"Finally! I don't have to Google 'what is an IBAN' every time I send money home. It just works like Venmo now."

"The instant transfer option saved me when I had an emergency. Worth every penny for the speed."

"As a support agent, my life is so much easier. I can see exactly where the money is and tell the customer confidently."

Lessons Learned

Perceived Performance > Actual Performance

Engineering pushed back on "Smart Routing" due to 800ms API latency. I compromised by proposing "Skeleton Loaders" and "Optimistic UI" updates, which kept the perceived friction at zero while the backend crunched the numbers.

Impact of "Plain Language"

Replacing "ACH" with "Standard delivery (1-3 days)" reduced cognitive load more than any visual change. It taught me that copywriting is the most high-leverage UX tool in fintech.

What I would improve next

Real-Time Tracking (SWIFT gpi)

Integrate SWIFT gpi data to provide minute-by-minute location of funds across intermediary banks.

AI Support Deflection

Deploy a corridor-aware chatbot to handle "Where is my money?" queries using live ledger data.

Smarter Validation

Implement AI-based typo detection for recipient names and account numbers based on corridor patterns.

Corridor Localization

Context-aware input fields that change dynamically based on local banking regulations (e.g., CLABE in Mexico).